Key Message

AEye’s *software-defined LiDAR makes it a technology innovator, yet the company is still in an early-revenue phase with persistent losses and extreme share-price volatility. The July 2025 announcement that its Apollo sensor is fully integrated into NVIDIA’s DRIVE AGX platform sparked a dramatic rally, but long-term financial sustainability remains uncertain.

1. Company Snapshot

| Item | Details |

|---|---|

| Founded | 2013 (Pleasanton, CA) |

| Employees | ≈ 45 |

| Listing | NASDAQ (LIDR) |

| Core Products | 4Sight™ Platform, Apollo LiDAR |

| July 2025 Milestone | NVIDIA DRIVE AGX full integration |

2. Technology Highlights

- Software-Defined LiDAR: Real-time, software-controlled scan pattern enables long-range (up to 1 km) high-resolution detection.

- Adaptive SmartScan: Automatically concentrates laser focus on areas of highest interest, boosting perception efficiency.

- OTA Upgrades: Features can be added without hardware swaps, reducing total cost of ownership.

- Compact 1550 nm Apollo Sensor: Designed for behind-windshield installation, simplifying OEM integration.

3. Financial Performance

| Fiscal Year | Revenue | YoY Growth | Net Loss | Notes |

|---|---|---|---|---|

| 2024 | $0.20 M | –86% | –$35.5 M | Limited to sample shipments |

| 2023 | $1.46 M | –60% | –$87.1 M | Cost-cutting begun |

| 2022 | $3.65 M | +21% | –$98.7 M | First commercial deliveries |

- End-2024 cash $22.3 M; quarterly burn ~$4.8 M ⇒ runway to mid-2026.

- Low debt, but equity raises may dilute shareholders.

4. Market Position vs. Key Rivals

| Company | Market Cap | Technology Focus | Differentiator |

|---|---|---|---|

| Hesai | $2.8 B | Hybrid/solid-state LiDAR | China OEM dominance |

| Luminar | $1.4 B | Solid-state + software | Volvo, Mercedes contracts |

| Ouster | $1.2 B | Digital LiDAR | Industrial diversification |

| AEye | $0.09 B | Software-defined LiDAR | NVIDIA DRIVE certification |

AEye is the smallest by capitalization but competes with a unique software-centric stack that can re-target beams in flight, a capability most rivals lack.

5. Strategic Pipeline

- NVIDIA DRIVE Ecosystem: Opens doors to global Tier-1 OEMs; accelerates production roadmap.

- LITEON Manufacturing JV: Plans for Apollo mass production in H2 2025.

- OPTIS Physical-AI Suite: Extends sensing tech to smart infrastructure and security verticals.

- China Partnerships: Pursues logistics and robotics customers via local alliances.

6. Investment Upside vs. Risks

| Upside Catalysts | Principal Risks |

|---|---|

| – NVIDIA endorsement lifts technical credibility and sales pipeline | – Revenue still < $1 M; commercial traction unproven |

| – Software-defined approach can undercut price/performance of fixed-scan rivals | – Continuous net losses; further share dilution likely |

| – Tier-1 production with LITEON readies volume supply | – Share price volatility (>200% annualized) complicates entry/exit |

| – Adjacent markets (smart traffic, security) expand TAM | – LiDAR ASP erosion & OEM adoption delays |

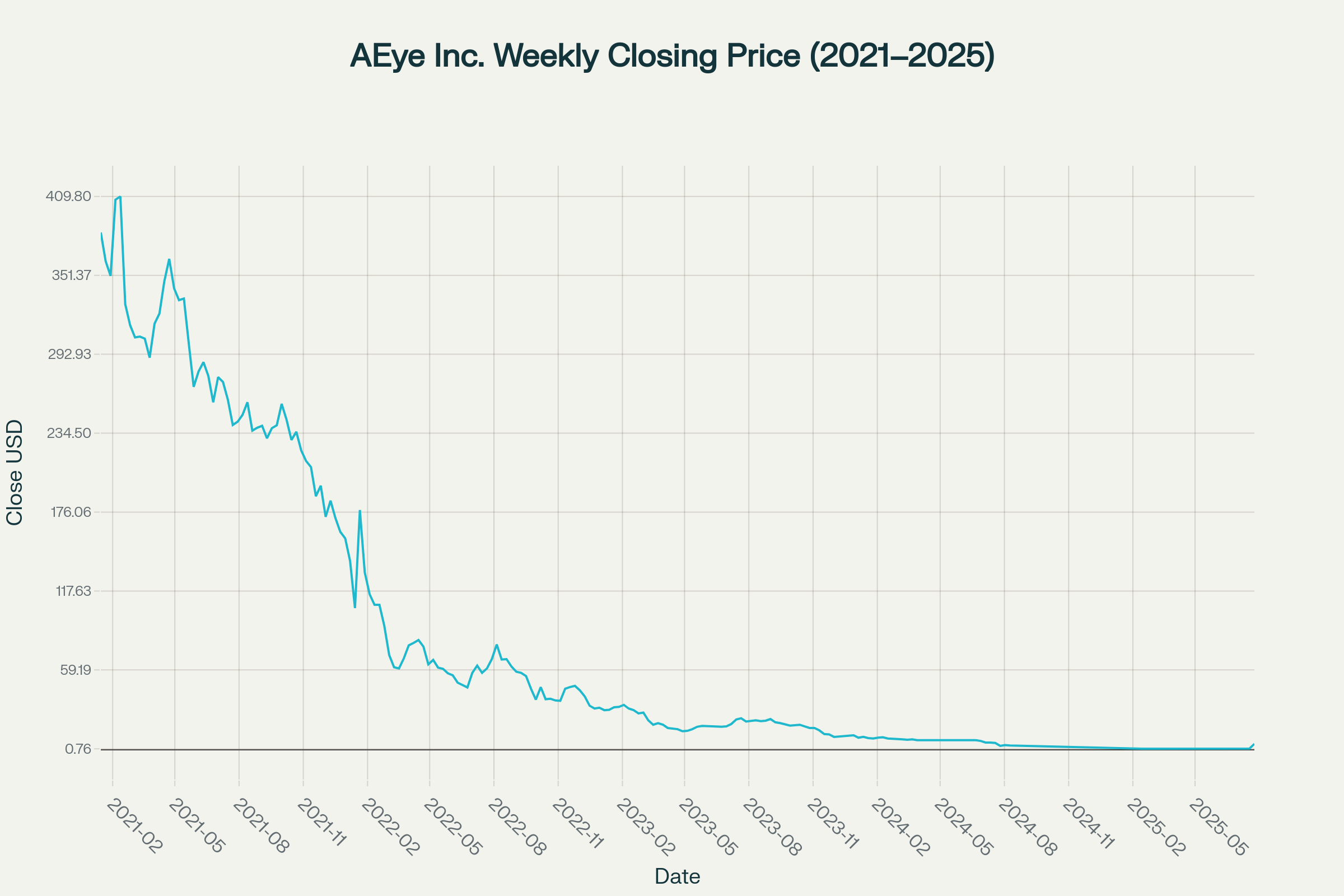

7. Stock-Price History (Weekly Close, 2021–2025)

AEye weekly closing price (2021–2025)

Graph Insight

- Early-2021 SPAC peak >$400 collapsed below $1 by early-2025 as commercialization lagged.

- NVIDIA integration news on 24 Jul 2025 triggered a 300% one-day spike to $4.43, breaking the down-trend but leaving valuation highly sensitive to execution milestones.

8. Conclusion

AEye’s breakthrough with NVIDIA substantiates its technology and could unlock OEM deals; however, its micro-scale revenue base and persistent losses mean execution risk is high. The next 12–18 months—covering Apollo mass-production readiness and first OEM launches—will determine whether the recent rally marks a sustainable turnaround or another speculative spike. Position sizing discipline and tight risk controls are essential for investors considering exposure.